Why Are Borrowing Costs So High for Developing Countries?

The Role of External Factors

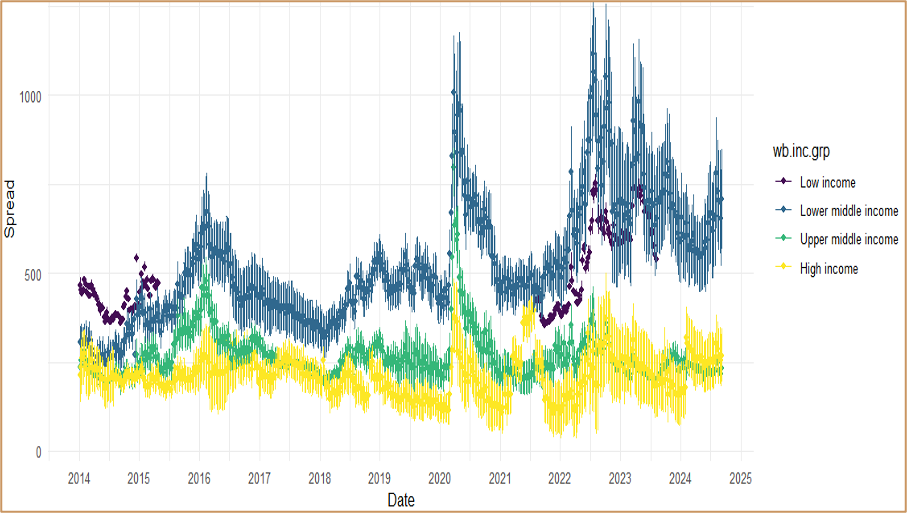

Over the past decade, borrowing costs for Low- and Lower-Middle-Income Countries (LLMICs) have risen sharply. In 2015, their Eurobond spreads were broadly in line with those of Upper-Middle-Income Countries (UMICs). Today, LLMICs’ spreads are three times higher and far more volatile—placing them in a separate asset class. This divergence raises urgent questions: Why has market confidence in LLMICs deteriorated so much? And why is the gap with UMICs widening, even though both groups face the same global shocks—such as the COVID-19 pandemic and rising U.S. interest rates?

Eurobond spreads for low and middle-income countries – 2014 to 2025

- LLMICs: Median spreads jumped from ~250 basis points in 2015 to ~750 in 2025, with much higher volatility.

- UMICs: Spreads briefly rose from ~250 to ~500 in 2023 before returning close to pre-crisis levels, with only modestly higher variability.

What explains the divergence?

The Paper shows that high borrowing costs are not only the result of domestic economic risks, but also of external systemic factors—from inflexible debt structures dominated by preferred creditors, to fragmented creditor groups that struggle to coordinate, and to a global financial safety net too shallow to stabilize shocks. We empirically examine three types of factors and assess their impact on borrowing costs.

- Debt inflexibility: The accumulation of IFIs’ debt stocks, with Preferred Creditor Status, makes total debt less flexible. We find that this contributes significantly to the rise in the spreads of both LLMICs and UMICs, but much more so for the former.

- Debt heterogeneity: Heterogeneous creditors face free riding incentives and have hard time coordinating the rollover of maturing debt and restructuring debt when needed. The lack of coordination is especially marked between private and Chinese creditors, as there is no history of cooperation among them. We find that this effect affects LLMICs more than UMICs.

- The Global Financial Safety Net (GFSN) is not deep enough to allow DCs to smooth adjustment costs and service external debts during market downturns. The surge in IFI lending has ended up refinancing commercial debts, not financing recoveries in LLMICs. In effect, loans from IFIs come with an opportunity cost. The accumulation of IFI debt makes external debt less flexible and commercial debt more expensive. Unless IFI loans generate growth, the net effect over time is more likely to be negative.

These dynamics mean developing countries often appear riskier than they truly are. For these countries, interest charges not only compensate for risks related to domestic debtor policies but also for additional risks generated by agency costs within the creditors' group itself. Moreover, many are “illiquid but solvent”: they could repay comfortably if debts were rescheduled, but high spreads make voluntary refinancing impossible. Worse, elevated borrowing costs can trigger self-fulfilling debt crises, as markets anticipate default.

What needs to change?

To reduce the external effects and lower the cost of borrowing, two problems need fixing:

- A deeper GFSN – to help countries smooth shocks and service debts without triggering crises.

- Fairer burden sharing – creditors must coordinate better when debts are sustainable but refinancing is blocked by market spreads.

The two solutions are complementary. Solving the first without the second would require a GFSN much larger than DCs’ market borrowings—many times bigger than what is currently available. Conversely, it is not possible to address the second challenge without a sufficiently large GFSN that has enough bargaining power to enforce cooperation.

Ensuring the IFIs' transfers do not leak out, but are used instead to improve growth, generates two types of gain: the debt burden comes down as countries are able to grow over their debt problem, and debt remains balanced between IFIs and commercial sources, leading to more gains in lower borrowing costs -- reinforcing the possibility for a return to voluntary refinancing.